Flooding is much more usual than several property owners realize, and the price of repair work can be considerable. Time after time, large numbers of flood-related cases would certainly drive costs greater for everybody and can even make insurance eligibility more difficult. It's all-natural to think that if floodwaters enter your home, your property owners insurance coverage should aid pay for the damage.

Flooding is much more usual than several property owners realize, and the price of repair work can be considerable. Time after time, large numbers of flood-related cases would certainly drive costs greater for everybody and can even make insurance eligibility more difficult. It's all-natural to think that if floodwaters enter your home, your property owners insurance coverage should aid pay for the damage.Your Standard Home Owners Policy Doesn't Provide Flood Protection

- Under the HO-3 policy type, personal property coverage normally represents 16 named hazards.

- Some kinds of storm damages are covered by many homeowners insurance plan, but some are not.

- Home owners' insurance is far from comprehensive, however there are a couple of kinds of tornado damage that practically every plan will certainly cover.

- This insurance coverage can help you pay to fix or change things that are harmed or damaged by a protected event, or which are swiped (see listed below).

Note that if, throughout the life of the finance, the maps are revised and the building is now in the high-risk area, your lender will inform you that you must buy flooding insurance coverage. A private flooding insurance plan commonly does offer coverage for Additional Living Costs. A personal flooding insurance plan generally covers sump pump failing if flood is the reason for the fall short.

The risk has to be detailed in your policy to be taken into consideration a covered case. Note that flooding damages is generally omitted under a typical home owners insurance coverage. You'll usually require a different flood insurance policy for this type of protection. Water damage brought on by flooding is not covered under a typical home owners insurance plan. Furthermore, water damage caused by a sewer backup, inappropriate setup of a home appliance, or absence of maintenance (i.e., pipes) will not be covered.

What kind of water damage is not covered by house owners insurance?

Flooding is the No. 1 natural catastrophe in the USA, yet homeowners insurance policy does not cover this peril. Generally, any type of water that moves into your home from the ground isn't covered. So rain, a surging river and saturated ground aren't covered.

Will My Insurance Plan Pay For Damage From A Drain Back Up Into My Cellar During The Flooding?

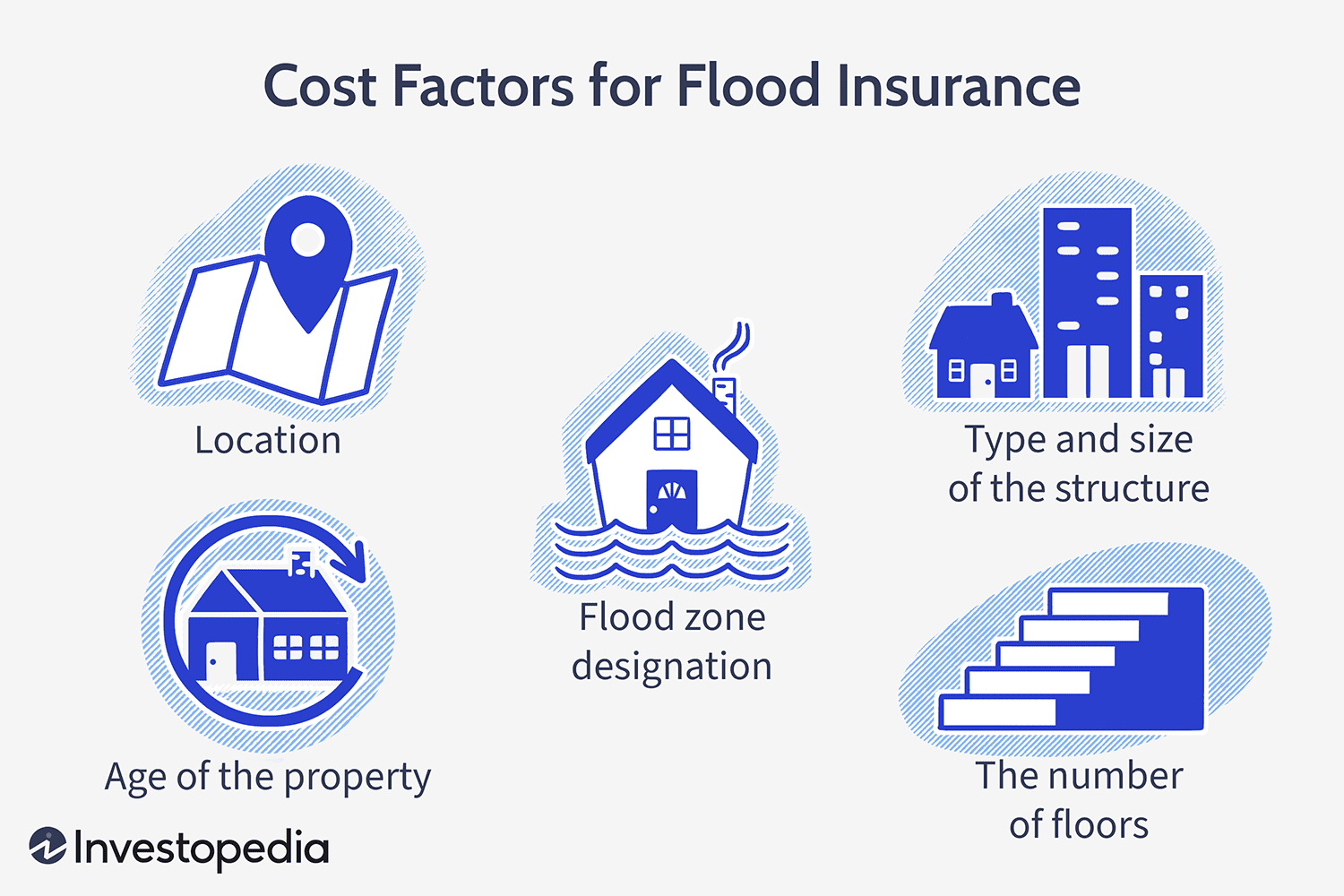

Personal property protection, nonetheless, normally does not encompass damages triggered by wild pets. Flooding happens in modest- to low-risk locations along with in risky areas. Poor drain systems, rapid accumulation of rainfall, snowmelt and broken water pipe can all cause flooding. Properties on a hillside can be damaged by mudflow, a protected peril under the Criterion Flooding Insurance Coverage. In high-risk locations, there is at least a one-in-four chance of flooding throughout a 30-year mortgage. For these reasons, flooding insurance is called for by law for buildings in high-risk flooding areas as a condition of obtaining a home loan from a federally managed or insured lending institution.

Flooding can take place in many methods, consisting of hefty rains, tornado rises, or overruning rivers. If floodwaters harm your home, you'll need a separate flood insurance plan to cover the repair service costs. Without flood insurance policy, you'll be in charge of spending for the damage expense, which can quickly become overwhelming. According to the Federal Emergency Situation Management Company (FEMA), just 1 inch of floodwater in your house can create greater than $25,000 in damages. While floodings are one of the most common all-natural catastrophe in the United States, Coverage dispute insurance coverage for losses from floods is not offered in common property owners or lessees policies. Insurance for flood damages is normally readily available under a separate policy provided via the National Flood Insurance Program (NFIP) and readily available to homeowners, renters and organizations.

Dropped Trees

Either kind can use wonderful coverage, but the very best option for you will depend on a range of elements. That being claimed, some plans especially leave out damages caused by winds. This is a lot more typical in areas vulnerable to solid hurricanes, such as cyclones and tornadoes. If your policy does not automatically include Coverage dispute for wind damage, it might be feasible to include a wind damages rider. Numerous exclusive insurer offer Excess Flood Protection, Coverage dispute which provides limits over and above those of the NFIP. Also if flood insurance isn't required by your lender, it's worth examining your flood danger to establish whether you need protection.